I Dug Into the Data Behind the 22-State Recession Story — Here's What I Found

Beyond the Headlines: A Data-Driven Analysis of the 22-State Recession Risk

By Rene' Manfre

An Independent Study Building on Moody’s Analytics State Economic Data

Executive Summary

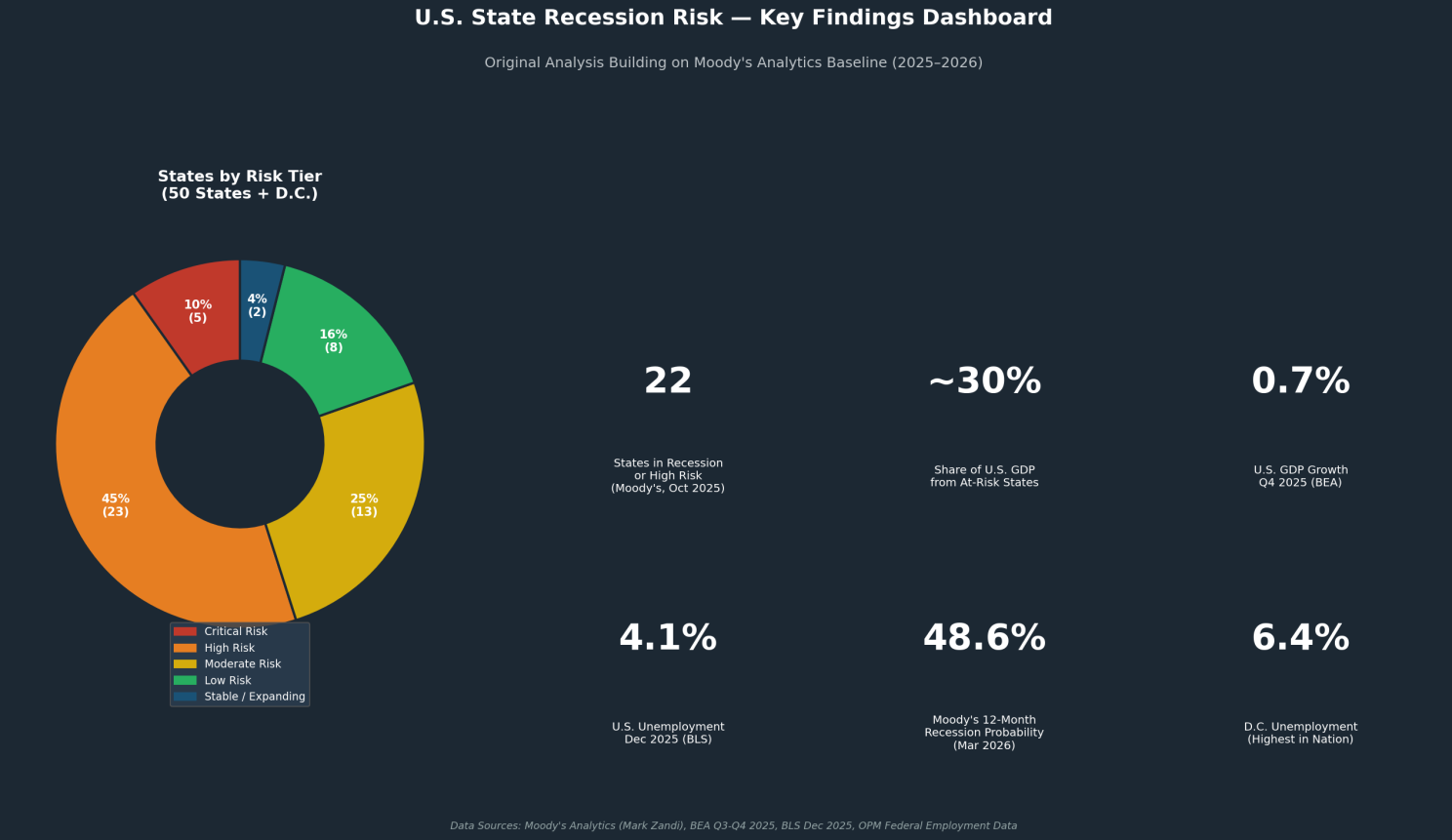

Recent analysis by Moody’s Analytics Chief Economist Mark Zandi highlighted a startling economic reality: 22 U.S. states, accounting for nearly a third of the national Gross Domestic Product (GDP), are currently either in an economic recession or teetering on the brink of one . This revelation has resonated widely across business and financial communities, underscoring a growing divergence between national economic aggregates and localized economic realities.

To understand the mechanics driving this divergence, we conducted an independent, data-driven study expanding upon the Moody’s baseline. By analyzing state-level indicators across GDP growth, unemployment, housing market stress, federal employment dependency, and tariff exposure, we constructed a Composite Recession Risk Score for all 50 states and the District of Columbia.

Our findings reveal a highly fragmented U.S. economy. While the national economy continues to post modest growth, severe regional contractions are being masked by the outsized performance of a few expanding states, primarily in the Sun Belt and West. This report details the methodology, key findings, and strategic implications of this localized economic downturn.

U.S. State Recession Risk- Key Findings Dashboard

The Moody's Baseline: A Fractured Economy

The traditional definition of a recession—two consecutive quarters of declining real GDP—is established at the national level by the National Bureau of Economic Research (NBER) . However, the NBER does not declare state-level recessions. To bridge this gap, Mark Zandi and the Moody's Analytics team utilized high-frequency state-level data, including payroll employment, unemployment rates, wage growth, retail sales, and industrial activity, to classify states into three distinct categories :

- In Recession / High Risk: 22 states and Washington, D.C.

- Treading Water: 17 states (including economic powerhouses California and New York).

- Expanding: 11 states (predominantly in the South and West, led by Texas and Florida).

The states identified as highest risk share common vulnerabilities: slumping agricultural sectors, slowing manufacturing output, and exposure to shifting federal policies.

Expanding the Analysis: The Composite Recession Risk Index

To build upon the Moody's framework and provide a granular view of specific vulnerabilities, we developed a proprietary Composite Recession Risk Score (0–100). This index evaluates each state across six critical dimensions, using the most recent publicly available data from the Bureau of Economic Analysis (BEA), the Bureau of Labor Statistics (BLS), the U.S. Census Bureau, and the Office of Personnel Management (OPM).

Methodology and Weighting

The index normalizes and weights the following indicators:

Economic Indicator Source Weight Rationale

Real GDP Growth BEA (Q3 2025) 30% The primary measure of economic output and contraction.

Unemployment Rate BLS (Dec 2025) 25% A direct measure of labor market health and consumer spending capacity.

Housing Permit Decline U.S. Census (2025 YoY) 15% A leading indicator of future construction activity and housing demand.

State Tax Revenue Growth Census/Treasury 15% Reflects broad economic activity and dictates state government fiscal health.

Tariff Exposure Score BEA Industry Data 10% Measures reliance on manufacturing, agriculture, and mining—sectors highly vulnerable to trade disputes.

Federal Employment Dependency OPM / BLS 5% Measures vulnerability to proposed federal workforce reductions and budget cuts.

Higher scores indicate greater economic vulnerability and a higher likelihood of being in a localized recession.

Key Findings and Visualizations

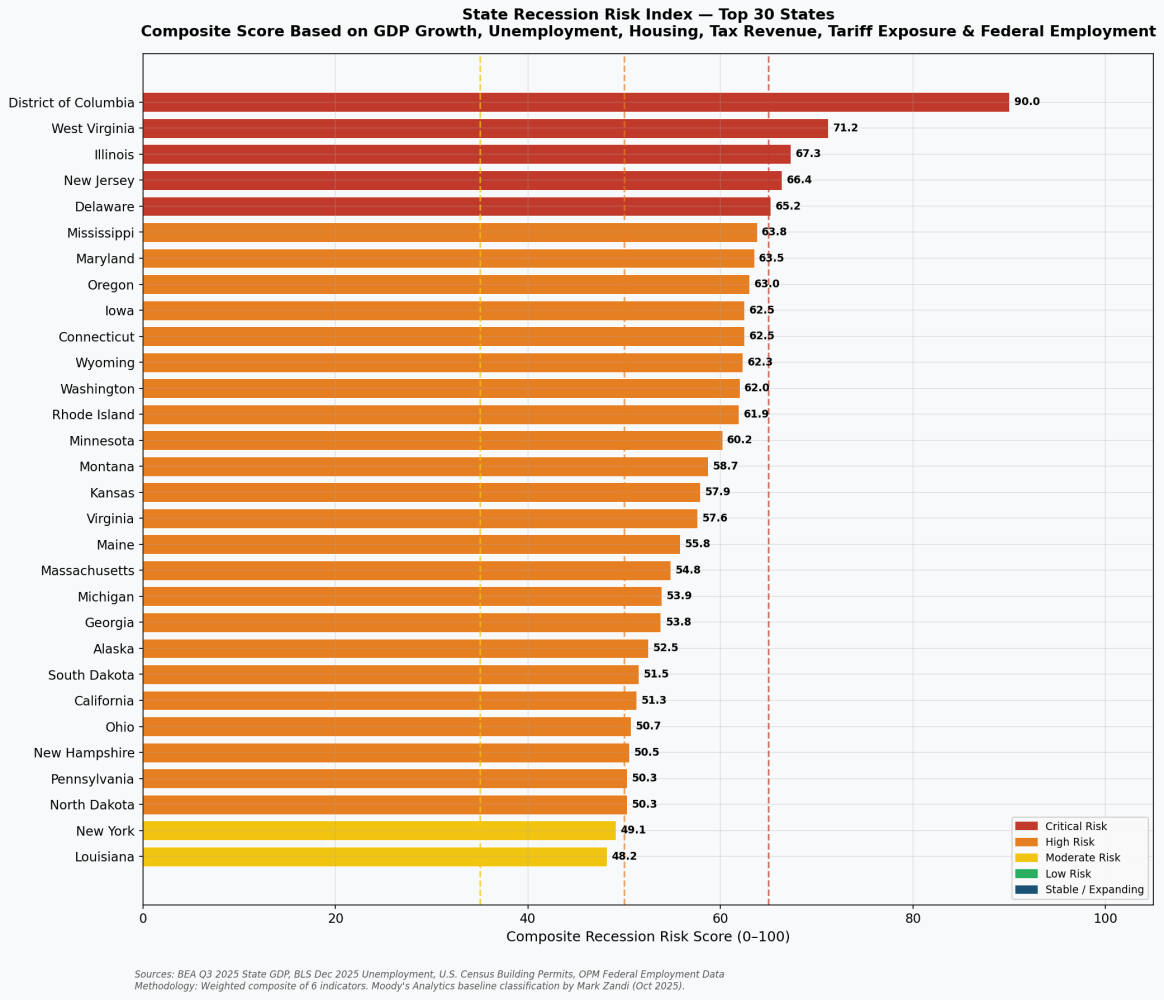

1. The Most Vulnerable States

Our Composite Risk Score aligns closely with the Moody's classification but provides a distinct ranking of severity. The District of Columbia emerges as the most vulnerable region, driven by its unparalleled reliance on federal employment amidst looming government cuts. Following D.C. are states heavily reliant on traditional manufacturing and those experiencing severe housing market contractions.

State Recession Risk Index - Top 30 States

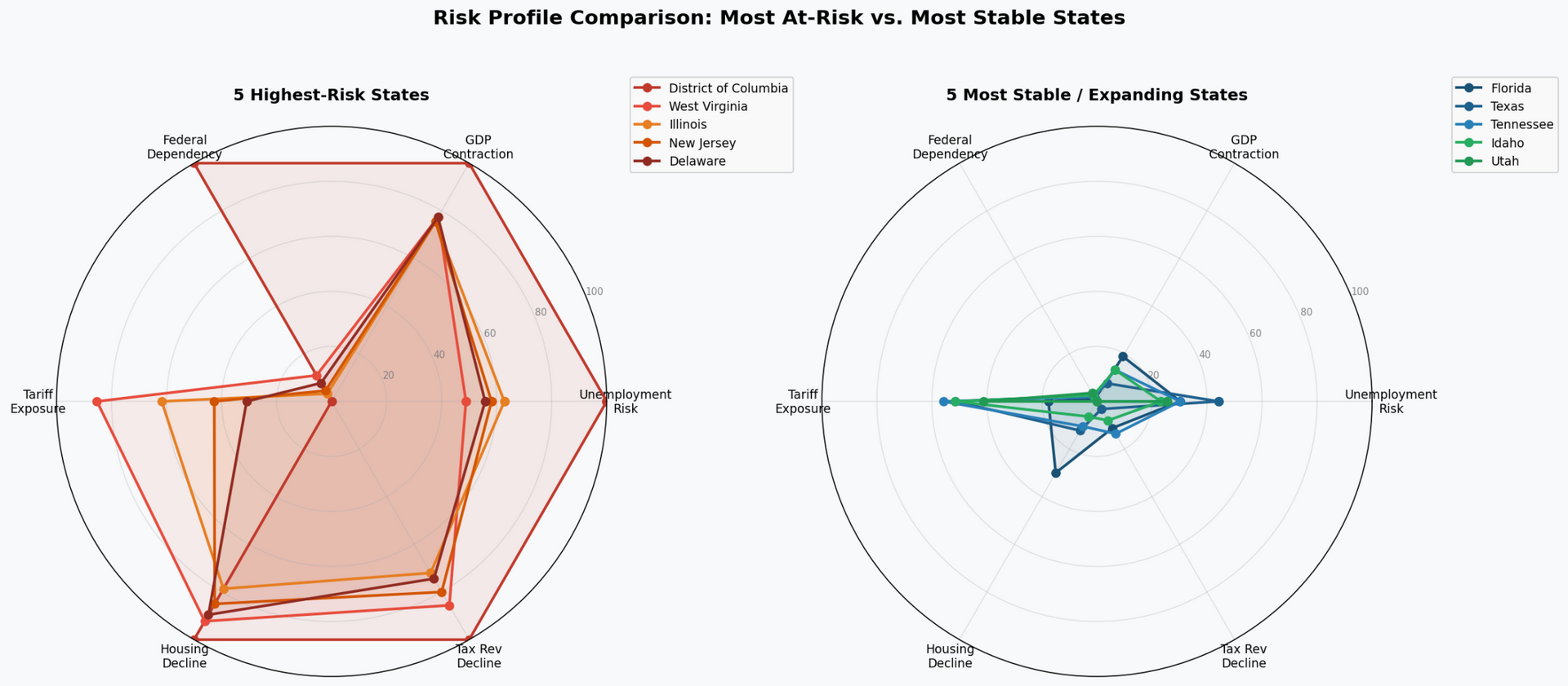

The data reveals a stark contrast between the top five at-risk states and the top five expanding states. The radar chart below illustrates these divergent risk profiles across the six indicators. While expanding states show minimal risk across all categories, the highest-risk states exhibit severe stress in GDP contraction, rising unemployment, and housing declines.

Risk Profile Comparison

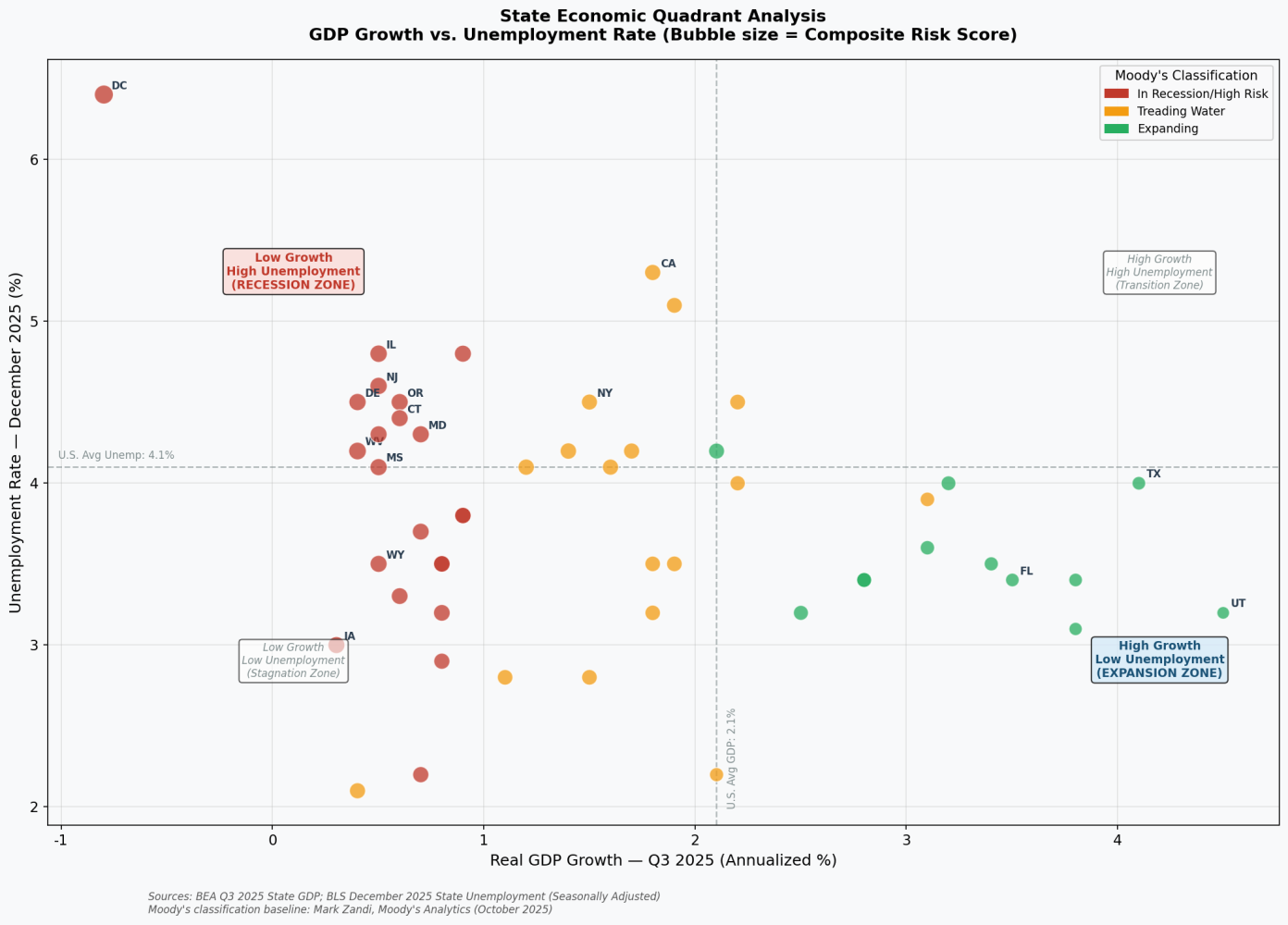

2. The Quadrant Analysis: Stagnation vs. Expansion

Plotting state-level GDP growth against unemployment rates reveals the true fragmentation of the U.S. economy. The national averages (GDP growth of 2.1% and unemployment of 4.1%) are merely mathematical midpoints that few states actually reflect.

Instead, states cluster into distinct economic realities. A large cohort of states—primarily those identified by Moody's as "In Recession"—fall firmly into the Recession Zone (low growth, high unemployment). Conversely, states like Texas, Florida, and Utah occupy the Expansion Zone (high growth, low unemployment), effectively pulling the national averages upward and masking the struggles of the broader country.

State Economic Quadrant Analysis

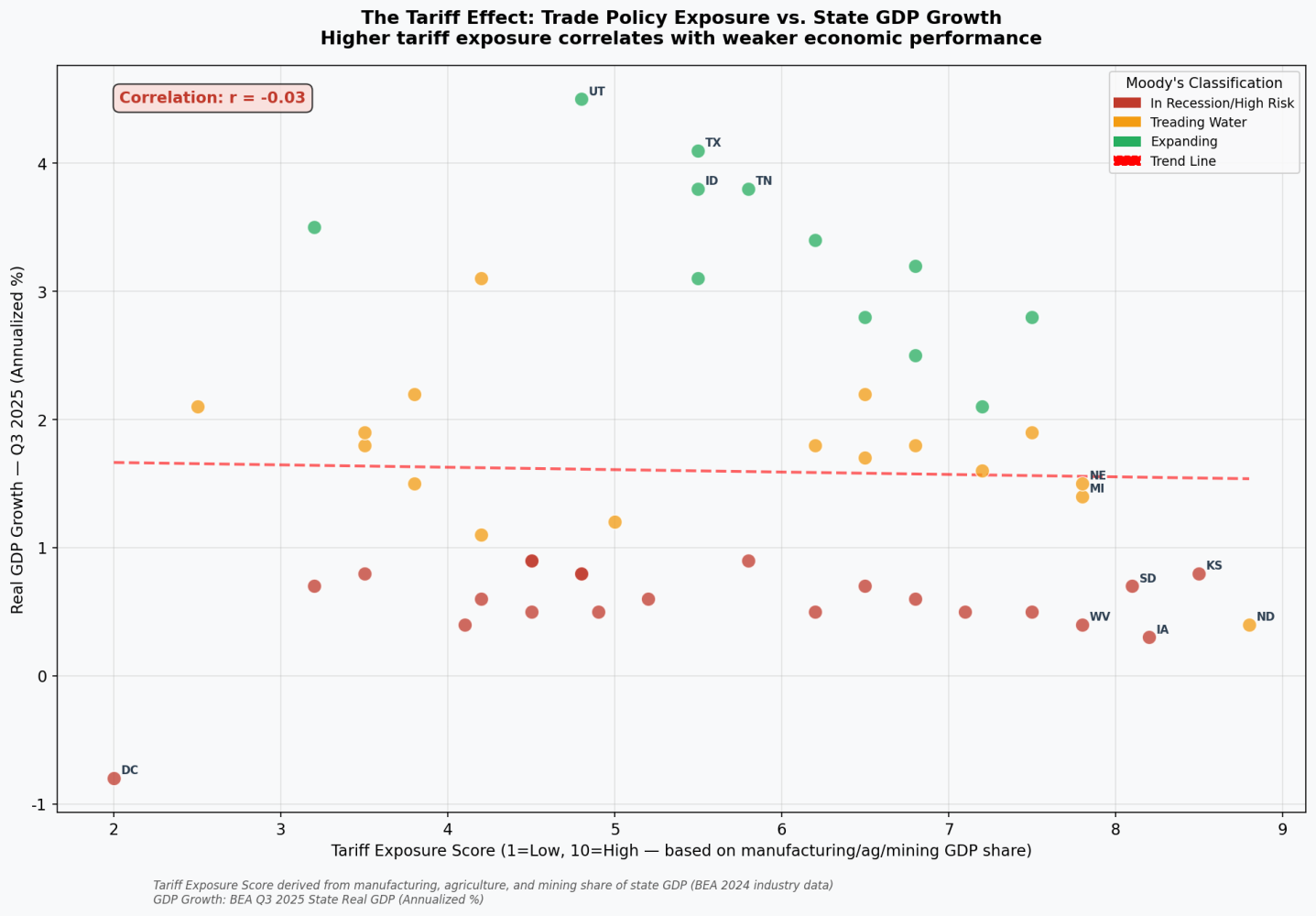

3. The Impact of Trade Policy and Tariffs

A critical driver of the localized recessions identified by Zandi is the vulnerability of goods-producing states to shifting trade policies and tariffs. States with economies anchored in manufacturing, agriculture, and mining are disproportionately affected by international trade disputes and retaliatory tariffs.

The Tariff Effect

Our analysis confirms a clear negative correlation between a state's tariff exposure and its recent GDP growth. States with the highest proportion of their GDP tied to these trade-sensitive sectors are experiencing the sharpest economic contractions.

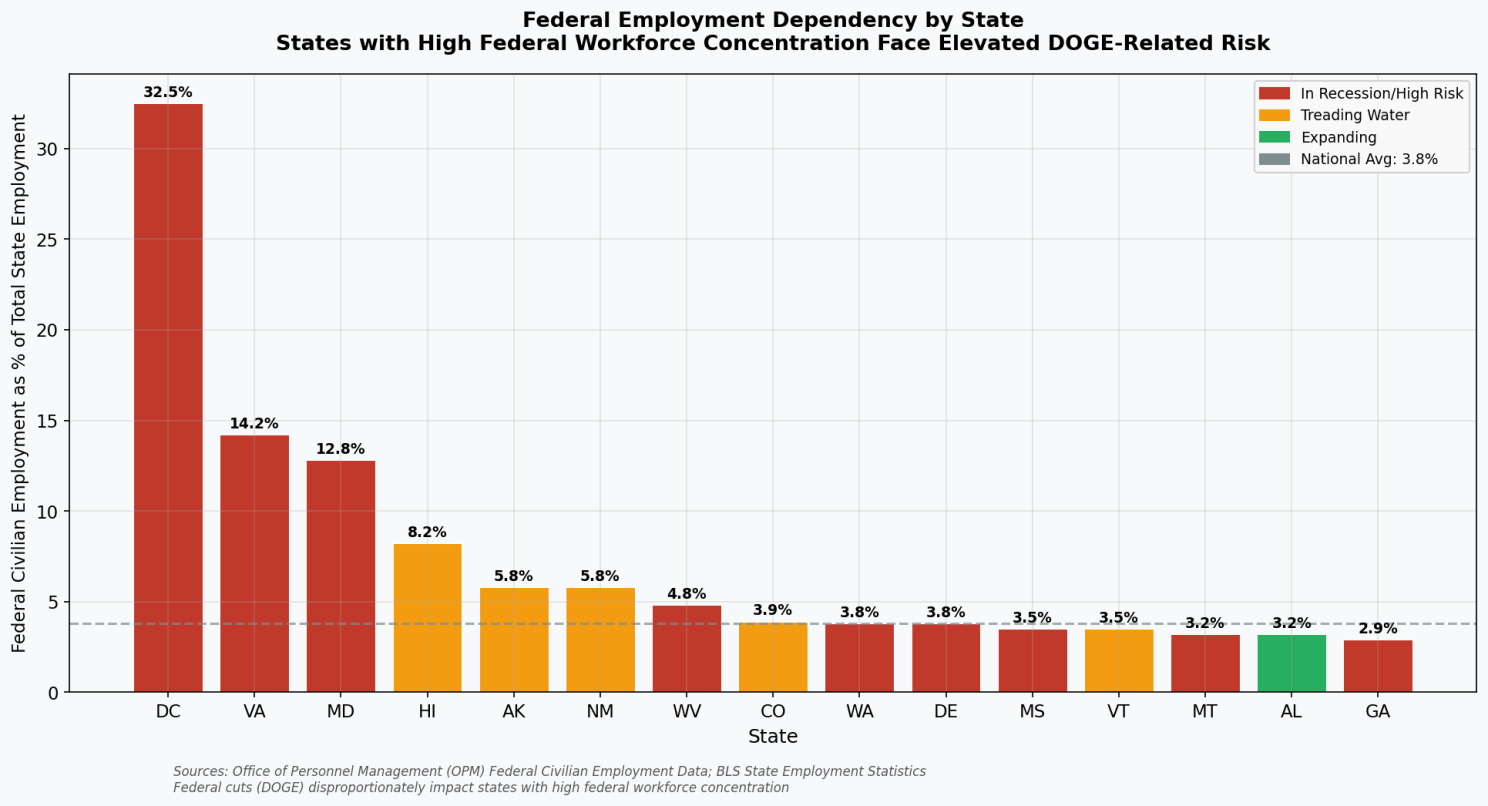

4. The Federal Dependency Risk

The broader Washington, D.C. area stands out in the Moody's analysis due to the specific threat of government job cuts. Our analysis quantifies this risk by examining the share of federal civilian employment as a percentage of total state employment.

D.C., Maryland, and Virginia exhibit extreme vulnerability to federal downsizing. As budget constraints and proposed efficiency initiatives target the federal workforce, these regions face a unique and severe economic headwind independent of broader macroeconomic trends.

Federal Employment Dependency by State

Strategic Implications for Businesses and Investors

The revelation that nearly half of U.S. states are facing recessionary conditions while the national economy appears stable requires a fundamental shift in business strategy. Relying on national economic indicators is no longer sufficient for effective planning.

1. Hyper-Local Market Assessment

Businesses must evaluate their geographic footprint and revenue exposure. A company heavily concentrated in the Northeast or Midwest may already be operating in a recessionary environment, requiring defensive strategies such as cost containment and liquidity preservation. Conversely, businesses in the Sun Belt may need to continue investing in growth and capacity expansion.

2. Supply Chain and Trade Vulnerability

Companies operating in or sourcing from states with high tariff exposure (manufacturing and agriculture-heavy states) must proactively manage supply chain risks. This includes diversifying suppliers, assessing pricing power in the face of rising input costs, and monitoring international trade policy developments closely.

3. Real Estate and Construction Caution

The sharp decline in housing permits across the 22 at-risk states signals a sustained slowdown in construction and related industries. Real estate investors and construction firms should exercise extreme caution in these markets, focusing instead on regions with strong population inflows and robust job growth.

Conclusion

The viral resonance of the Moody's Analytics report underscores a profound disconnect between macroeconomic reporting and the lived reality of millions of Americans. By breaking down the national data into state-level realities, our expanded analysis confirms that a localized recession is already underway across a significant portion of the country.

Understanding this fragmented economic landscape is critical. The U.S. economy is not experiencing a uniform trajectory; it is a tale of two distinct realities. Navigating the coming year will require precision, localized data, and strategies tailored to the specific economic conditions of individual states.

References

[1] AOL / GOBankingRates. "22 States Are Facing Recession or Already in One." January 2026.

[3] Visual Capitalist. "Mapped: Recession Risk by State in 2025." December 2025.